It is clear that a shortage of domestic containers limited intermodal gains in fourth quarter 2017. Data show that even while truck spot rates soared to record levels and trailer-on-flatcar 53-foot trailer loads shot up nearly 14 percent year over year in December, domestic container activity inched up only 1.2 percent. This trend, in place for the last few months, clearly indicates that the culprit was not enough boxes or, at least, not enough boxes in the right places. A closer look, however, reveals there is a bit more to the story.

{kind=link}

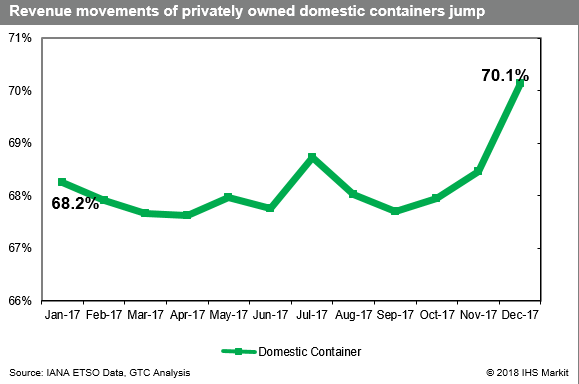

This chart from our new Intermodal in Depthnewsletter shows that in recent months there has been a significant change in the texture of the domestic container intermodal market. Using data from the Intermodal Association of North America, the share of revenue movements by privately owned (versus rail-owned) domestic containers has broken a pattern of stability and moved up meaningfully in recent months.

Of the big Class I railroads, only BNSF Railway does not provide rail-owned boxes to a portion of the intermodal market. The principal fleets are EMP (principally Union Pacific and Norfolk Southern) and UMAX (principally Union Pacific and CSX). In addition, Canadian National Railway and Canadian Pacific Railway also operate rail fleets, but these mainly run domestically within Canada in support of their retail intermodal operations. The UMAX and EMP fleets collectively total well over 84,000 boxes, representing about one-third of the US dry domestic container fleet.

If we look at fourth quarter 2017 intermodal activity just on US lanes, pulling out any volume moving cross-border or within Canada and Mexico, the difference is substantial. Revenue movements of privately owned domestic containers were up 4.8 percent year over year, while equivalent movements of rail-owned boxes declined 2.5 percent over the same time frame. Had the rail fleets performed as well as the private fleets, some 32,500 more intermodal revenue moves would have occurred in the fourth quarter. Put another way, that is 116 more full-size 280-container trains.

However, the comparison is not a fully clean one. The data capture any movement of private rail containers, whether they are loaded or empty, as long as there is rail revenue associated with the move. In contrast, if a rail-owned box moves empty, it is not captured in the data. If a large increase in empty moves occurred in the fourth quarter, that would have shown up as an increase for private boxes but not for rail containers. However, there is no indication that this actually occurred in the fourth quarter.

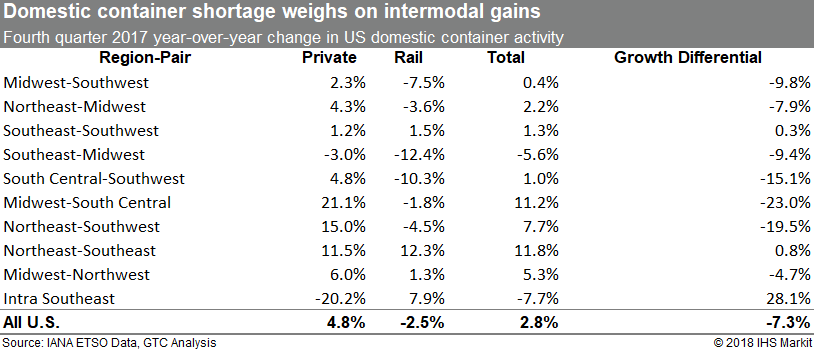

The situation is examined in more detail in the second chart. Looking at the 10 US region-pairs with the largest flows of domestic containers in the fourth quarter, several conclusions can be drawn. First, the issues with rail-owned boxes were not confined to one region or, by inference, one railroad. Second, the situation varied by lane. In many lanes the difference was truly dramatic, with a total growth differential at or above 10 percent. The most extreme differences can be seen in the Midwest-South Central (Texas) and Northeast-Southeast lanes, where the differential was at or above 20 percent. But there were also a couple of lanes where rail box movements performed better than private container movements. Third, also of interest is the strong performance for rail and private domestic containers in the Northeast-Southeast region-pair. North-south lanes appear to have fared better in general than east-west lanes.

{kind=link}

Some of the private-rail differential may stem from greater investment in additional capacity by the private fleets. But that does not explain why the volume moving in rail-owned boxes actually declined from the prior year. Clearly, there were some situation-specific issues in play that were impeding the velocity, free flow, and productivity of the rail-owned fleet(s).

The underlying message is, in a sense, positive. After operations return to normal and equipment starts flowing freely again, the capacity of the domestic container fleet should improve. This means that the railroads, in some respects, hold the destiny of the 2018 intermodal year in their hands. By decongesting the network and returning equipment velocity to previous levels, they can regain substantial fleet capacity without spending another cent. This is capacity that will be put to good use meeting the strong demand anticipated over the course of this year.