The under-performance of the US rail-owned domestic container fleet in the fourth quarter of last year led to domestic intermodal missing out on some of the opportunity presented by the tight US trucking market. But there is good news to report, at least based on February data. It looks like the rail-owned domestic container logjam has broken and velocity is beginning to return to normal. With boxes flowing more smoothly at normal speeds, additional intermodal capacity has been created, providing shippers with a better intermodal “safety valve” to help relieve the pressure built up by the tightening trucking market. It is vital that intermodal continues to perform up to its maximum capabilities now that it is entering the normal seasonal upswing in volume and full enforcement of the electronic logging device mandate has commenced.

Click to enlarge

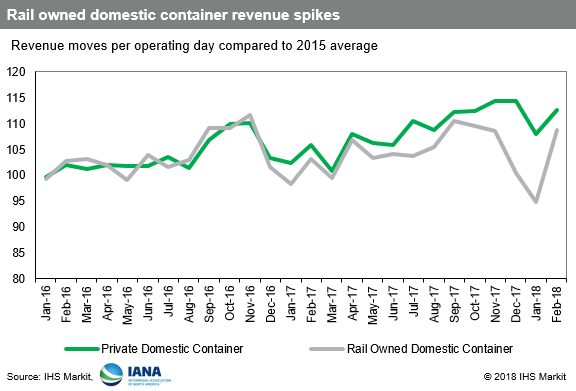

Click to enlargeEach month, the Intermodal Association of North America comes out with its Equipment Type/Size/Ownership data. Among many other aspects, this data permit the tracking of rail-owned versus private domestic containers and provide the basis for this analysis.

Exhibit 1 looks at the revenue moves per work day for rail and private domestic containers from February of this year and going back to the beginning of 2016. By using working days per month, the weekend timing effect can be washed out as well as the differing number of days per month of the year. In this chart, the average per work day for 2015 is set at an index of 100, and the chart then compares each month’s results versus this index. This approach also accounts for the revenue difference between privates and rail boxes, wherein even empty private domestic container moves are counted because there is usually rail revenue associated with the move, while empty rail box moves, with no revenue attached, are not covered. In looking at the chart, keep in mind that there are roughly twice as many private domestic container moves as occur in rail-owned boxes.

Exhibit 1 shows that rail-owned containers kept pace with privates all the way through 2016. Activity levels rose in a normal seasonal fashion as the second half of the year approached, topping out in the fourth quarter during the holiday peak. While there was normal variance from month to month, private containers (in green) and rail containers (in gray) remained in tight alignment throughout the year.

Such was not the case in 2017. Rail-owned containers lagged behind private domestic boxes throughout the year. After a slow start to the year, revenue moves per day in private domestic containers began a steady rise, topping out in November and December. The fact that volume per working day was virtually unchanged from November to December is likely an indication that the private domestic container fleet was maxed out during those months, with each box moving just as fast as operating conditions allowed.

The statistics for the rail-owned domestic box fleet tell a different story. Activity per day lagged behind the gains seen on the private side for most of the year. Only March and April were close. Things really started to go downhill after September. Revenue moves per operating day in rail-owned boxes actually declined in October and again in November, in defiance of normal seasonal trends. Then volume fell off the edge of the table in December and repeated the performance in January. The gap between privates and rail-owned boxes was widest in January, indicating the issue was most severe during the month.

But the news is better in February. Revenue moves in rail boxes per working day have bounced back sharply. Although still not fully in sync with private boxes, the gap has narrowed greatly. After the problems of December and January, rail-owned box productivity appears to be much improved.

This is significant because it is an indicator the intermodal operations returned to normal in February and that the network capacity was restored. With domestic containers moving at a normal pace, more capacity was created in February without adding a single new box. With the US trucking market conditions still very tight, shippers are looking for every avenue possible to get their freight moved.

Only time will tell if this initial trend can be sustained. Based on anecdotal reports, March was pretty rough, especially in Chicago. When the March data come out, the industry may see downward pressure on rail and private domestic container velocity. For the longer term, it can expect moves per working day to improve, if only because more boxes will likely be added to both fleets in order to meet the current demand. It is unlikely, however, that enough boxes will be added to either fleet to permit volume to grow if equipment velocity slows further. All eyes, therefore, will be on the intermodal network and whether it can retain its operational stride in the coming months.

As seen on