Larry Gross, president and founder, Gross Transportation Consulting, and JOC analyst | Jun 09, 2021 11:18AM EDT

While the current surge in import TEUs is of historic proportions, when the books are closed on 2021, the gains versus the prior year will not look nearly as strong, and will more closely resemble the gains seen in the year after the Great Recession.

A review of past performance for the years after the big year of recovery suggests dramatically slower growth in the future. Further, there is good reason to expect that the gains this time will trail those we have previously seen.

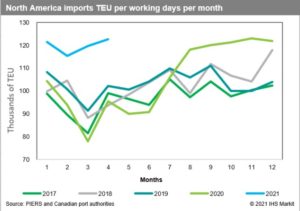

The first chart examines the import TEUs arriving in the ports of the US and Western Canada since the start of 2017. It portrays the TEUs per working day received each month. This approach removes a substantial amount of month-to-month volatility, which is a statistical artifact resulting purely from calendar effects.

We can see that in August of 2020, import TEUs shifted into a higher gear than has previously been seen. Activity has subsequently been sustained at roughly the same level. As we compare this period with prior years, we can see that not only has volume been strong, but also unnaturally stable. You normally don’t get six months of activity remaining within such a narrow range. Only February showed much differential, and we can easily attribute that to the polar vortex and associated operational disruptions.

Such flat activity suggests that the system has been bumping into its capacity ceiling. Barring new capacity being brought online or major improvements in velocity, there is little reason to expect this situation will radically change in the coming months. This implies that year-on-year gains are going to shrink dramatically come August no matter how strong demand is.

As shown in the second chart, the first four months of 2021 have produced an outsized 27.8 percent gain versus the prior year, which dwarfs 2020’s pandemic-impacted volumes. The last nine months have been exceptional by any measure. The gain has been over 20 percent versus the prior year. But how meaningful is this?

In 2010, import TEUs climbed 17.1 percent for the full year as we recovered from the Great Recession downturn the previous year. Subsequent years showed gains of less than 5 percent. If we assume that import TEUs continue to arrive at the same rate that they were received in April, then for the year 2021, we will see a gain for the year of slightly over 15 percent versus 2020. Will history repeat?

From 2010 through 2019, the last “normal” year, import TEUs grew at a compound annual growth rate of 4.5 percent. Volume has grown faster than GDP as a result of continuing offshoring activity. Importantly, this differential implies the continuing flow of jobs overseas. Given the current tensions with China and the disruptions importers are currently dealing with, offshoring additional products and economic activity perhaps isn’t the “no-brainer” that it used to be.

If the situation simply stabilizes, then import TEU growth rates won’t exceed that seen in the goods portion of GDP. In other words, it doesn’t take “near-shoring” or “reshoring” to produce dramatically slower import growth. It simply requires an end to the flow of new activity overseas.

Caution is therefore indicated when looking at the durability of the current surge. Activity will likely be buoyed by continuing strong economic growth. But there is little reason to expect that the current torrid pace will continue as we move into 2022 and beyond.

Contact Larry Gross at lgross@intermodalindepth.com.